How to Budget for Business: A New Approach That Actually Works (+ Profits)

The secret to growing a profitable business and building wealth is learning how to budget the right way. Creating an effective plan for your money is often overlooked, misunderstood, and even resented - but I'm here to change the way you approach business budgeting.

The REAL Reason You Need a Budget

I know how a lot of people feel about the word “budget.” So let me debunk a few things about budgeting for you.

What They Say: “I can’t do that because I’m on a budget.”

What I Say: Don’t budget just because you need to restrict your spending.

What They Say: “I can’t make a budget because my income is unpredictable.”

What I Say: Don’t budget by trying to project what you’re going to earn next month.

What They Say: “I keep blowing my budget, this isn’t for me.”

What I Say: Budgeting is not about measuring how many times you failed to stick to the plan.

Despite the fact that we have been taught these things, over and over again…

Budgeting is NOT synonymous with restriction.

Budgeting is NOT about forecasting and guesswork.

And budgeting is NOT a performance measure.

I want you to read this next sentence multiple times:

A budget should be a flexible plan for what you’re going to do with the money you currently have so that you can have the peace of mind that comes from giving yourself PERMISSION to use your money for intended purposes.

If that’s not the definition of budgeting you’ve been following, you’ve been doing it wrong. 😉

A New Perspective on Budgeting

Here is one major perspective shift on budgeting that will help you to quickly and easily start to adopt the definition I just gave you.

DON’T budget by sitting down on the first of the month and trying to guess what your numbers need to look like for the next 30 days. This just sets you up to fail, and few people find this helpful.

Instead, budget with the intention of proactively allocating REAL dollars to jobs.

Imagine This…

Imagine that you cashed out your entire bank account for physical money. Picture yourself sitting at your dining room table, sorting that money into piles for different purposes.

Maybe you put them into envelopes or buckets with labels for what that money is intended for. For example, Envelope #1 is for my software subscriptions, Envelope #2 is for my taxes, Envelope #3 is for my next paycheck to myself from my business.

Then, you accept a payment from a client. Now you have new dollars, and you can divide those up into your envelopes. Envelope #1 is fully funded, so you add to #2 and #3 but then put the rest into Savings Envelope #4 for your new laptop fund.

Paying a subscription? Take the money out of the envelope. Whatever’s left is what’s left for your other subscriptions. If you need more, you either need to earn more or move it from another envelope.

That’s the approach you need to take, even for digital dollars kept in an online bank! That’s how simple budgeting really is.

Your Step-By-Step Budget Routine

How do you choose which envelopes to fund?

When you approach budgeting this way, you usually won’t be able to fully fund a month the first time you do it. That’s why I don’t budget monthly.

I like to update my budget weekly on paydays. I’ve had seasons where I budgeted more consistently throughout the week as well.

(I never recommend budgeting less than once a week - you’ll lose the benefit of a proactive plan!)

When you budget week-to-week, your approach changes to funding your “envelope” categories in priority order.

1. Set aside 1-5% of your revenue for Profit savings

This is your emergency cash cushion. I recommend setting aside anywhere between 1-5% of your gross revenue for savings (start small and work your way up). Click here to read more about setting aside profit before you spend anything.

2. Set aside approximately 15% of your revenue for Tax savings

Many accountants teach you to set aside a % of net profit (after expenses) for taxes. I find it much simpler, and even safer, to set aside a % of your gross revenue (before expenses) instead. Always consult a tax professional for a personalized recommendation.

3. Set aside a percentage for your Owner's Pay fund

Even if you start small for now, be sure to pay yourself something out of your business.

The % you go with will vary widely based on personal need and goals.

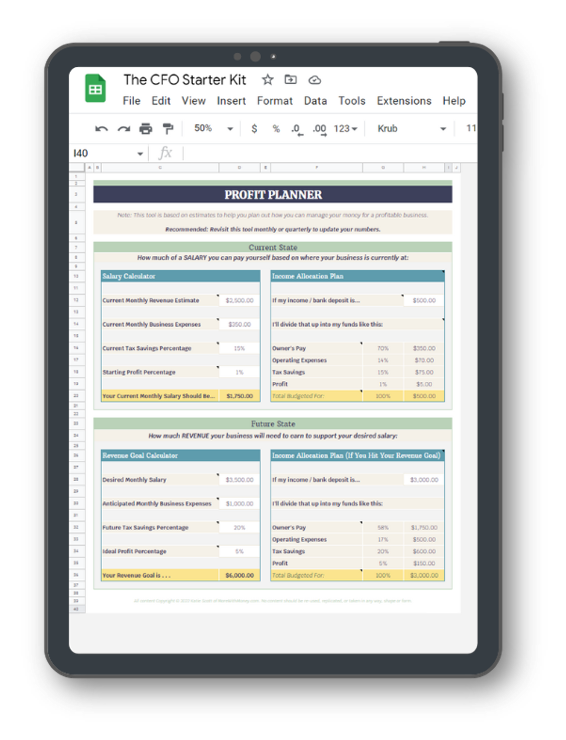

Use the future-state Profit Planner calculator inside the FREE CFO Starter Kit to determine your customized figure!

Click here to read more about How to Pay Yourself MORE from Your Business Today!

The Profit Planner found in the FREE CFO Starter Kit

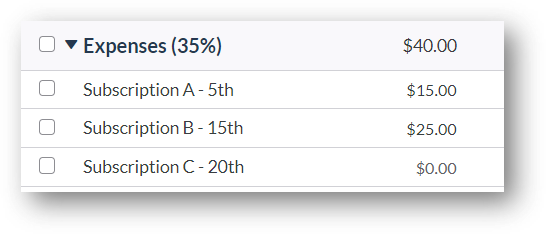

4. Fund monthly fixed expenses in chronological order

These are the regular costs you have each month where the amounts and due dates rarely change. Because these are coming out no matter what, you want to prioritize funding these in chronological order. My budget includes the date they’re due right in the name!

An example of fixed expenses in chronological order in the budget tool YNAB.

5. Fund monthly variable expenses in priority order

Then, your regular variable costs should be covered. These are still likely needed each month, but you typically have a little more control over the amount just in case you’re coming up short. (For example: office supplies, hourly contractors, books/education, food/meals, etc)

6. Fund your Sinking Funds

Brainstorm a list of everything you have that’s:

Infrequent (like annual subscriptions), or

Irregular (like ad campaigns or course purchases), or

Icky (like customer refunds or computer repairs)

These are your inevitables! Try to assign a dollar value to how much you’d ideally have set aside for this purpose. Total it up, divide by 12, round up - there’s your monthly sinking fund goal.

You CAN get more granular to track your savings for each individual fund (I do!), but you don’t have to start that way.

7. Fund future months

As you seek to stay ahead of all of the above expenses, eventually, you will find that you get further and further ahead of your bills. One day, you WILL be able to fund over a month ahead - that’s an amazing sign of cash flow security in your business (and your life, when you apply this to personal budgeting as well)!

How to Start Budgeting

You need to find a system that works for you to keep track of these different funds. I have a few different resources that I’d like you to check out so you can find what will work for you…

Option #1: Read The CFO Habits Series here on the blog - This series will walk you through a detailed business approach to tracking, planning, and analyzing your finances. Your budget is at the heart of all of that!

Option #2: Or, skip straight to The CFO Starter Kit - a high-value (but free) resource bundle that can get you started immediately on a spreadsheet approach to financial management. At the very least, it’ll TEACH you what you need in another system. Speaking of which…

Option #3: You can also jump straight into my favorite financial management tool, YNAB! - You Need a Budget (YNAB) is an incredible budgeting program that is extremely versatile for business owners and aligns with everything we’ve discussed today. You can try it for yourself here with my referral link OR read more about it here.

Are you ready to take your financial journey to the next level? Then you may be ready to check out the Cash Flow Strongholds! This course is THE money management system + fundamental financial literacy skills for entrepreneurs. If anything in this blog post piqued your interest, then this course is the perfect fit for you.

Pin for later

I'd love to continue the conversation in the comments! Feel free to share your thoughts.

Until next time!